Featured

Table of Contents

Decreasing financial obligation before using can enhance terms. Unlike some credit cards, personal loans usually do not have a coolingoff period; as soon as you sign, the loan is binding. A loan officer examines your application, discusses terms, and assists you browse the approval process. Yes. Joint applications can increase the approved quantity and improve rates if both applicants have strong credit.

Alternatives include credit cards with initial 0% APR offers, home equity credit lines, or loaning from family/friends. Online loan providers typically process applications within minutes, with funds disbursed in 13 service days after approval. Apply just through protected (HTTPS) websites, validate the lender's licensing, and prevent sharing passwords or PINs.

A difficult pull is a detailed credit query that takes place when you formally obtain credit; it can temporarily lower your score by a couple of points. Since individual loans are installment accounts, they don't straight impact credit usage, which only measures revolving credit use. Only if you have a solid repayment plan and the loan's APR is lower than alternative financing.

Pay attention to the APR, repayment schedule, costs (origination, late, prepayment), and any clauses about default. Students with a constant parttime or fulltime job and a decent credit history can qualify, though lots of lending institutions need a cosigner for younger debtors. Ontime payments improve your rating, while missed out on payments can cause considerable drops.

Finding Best-Rate Financing and Managing High Liability

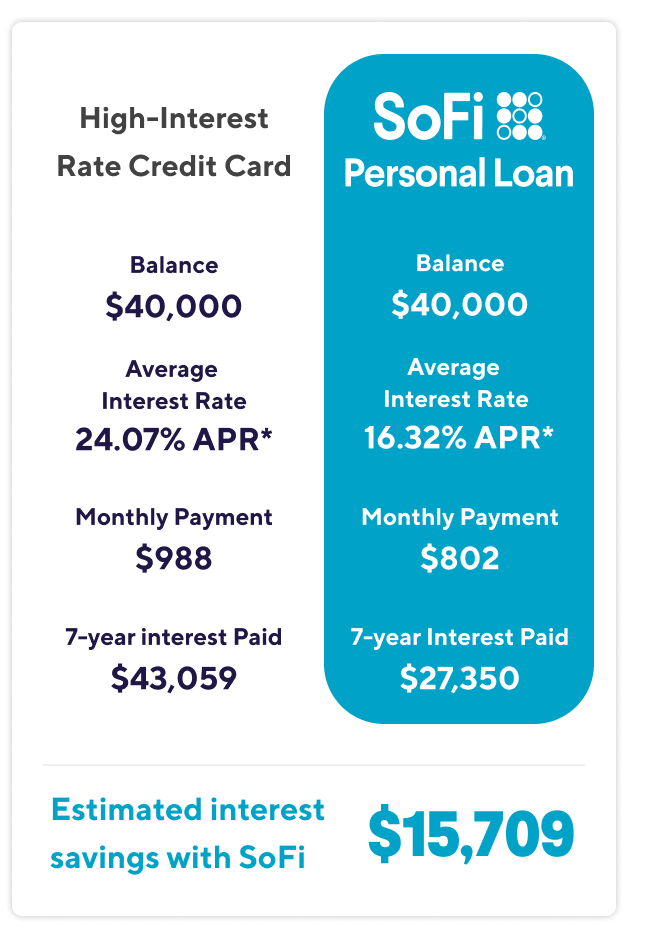

Some lenders may enable interestonly payments for a brief initial period, however this increases total interest paid. Terms usually range from 12 to 60 months, with some lenders providing to 84 months for larger loan quantities. Consolidating highinterest creditcard debt into a lowerAPR personal loan can reduce month-to-month payments and simplify finances.

Protected loans require security (like a cars and truck), which can reduce rates but put the asset at threat. Unsecured loans have no collateral, making them riskier for loan providers and frequently costlier.

Building a credit history first is suggested. Constant work shows repayment ability, frequently leading to much better rates and greater loan limitations. Yes, if you own a home with enough equity, a home equity loan might use lower rates, but you'll be putting your property at threat. Closing a loan early can decrease your credit mix and reduce your credit history, possibly reducing your rating somewhat.

Finding Competitive Private Financing in 2026

Inspect with VA-approved lending institutions. A soft check evaluates your credit without impacting your rating, permitting you to see possible deals before committing. While possible, service loans or SBA loans are usually better suited for organization financing due to much better terms and tax considerations. The brand-new loan's monthly payment is included to your existing debt obligations, raising your DTI.

Additional payments minimize principal much faster, decreasing overall interest and possibly reducing the loan term. Normally, personal loan proceeds are not taxable, however interest may be deductible just for certified business or investment uses.

Why Variable Rates May Be Risky for Your StateYes, but you might face higher rates or lower loan amounts. Structure credit through secured credit cards can assist before using. Borrowers with ratings above 740 often see APRs in between 5.99% and 9.99% on individual loans. Many do not; payments are due according to the schedule. Some lending institutions may offer a brief grace duration before examining late charges.

Utilize a spreadsheet to list APR, costs, loan quantity, term, regular monthly payment, and total expense. Inperson help can be handy for intricate scenarios, however online lending institutions often supply faster approvals and lower overhead expenses.

Optimal Strategies for Clearing Off Debt for 2026

Most individual loans are fixedrate, however a couple of lenders may offer variablerate choices tied to an index like the prime rate. Inspect the loan agreement for any earlyrepayment charges.

While the federal government does not supply unsecured personal loans, particular state programs might use lowinterest loans for particular purposes like education or catastrophe recovery. Preserving a loan in excellent standing for numerous years can positively affect your credit mix and payment history, boosting your score. Yes, combining payday advance into a personal loan can dramatically reduce the APR and get rid of predatory fees.

Some fintech platforms run promos with decreased charges or lower initial rates for new customers. Always read the small print. Greater inflation often leads to greater rate of interest as lending institutions change to keep genuine returns. Research study the loan provider, read reviews, and validate licensing. Offers with very low rates and no credit check are typically scams.

Expert Reviews On Financial Management Solutions for 2026

Obtaining $15,000 at 22% APR instead of 9% costs you an extra $3,200 in interest over 3 years. That difference comes down almost totally to your credit rating and which lending institution you walk into and most Americans accept the very first deal they get instead of shopping. Here's what the 2026 individual loan market in fact looks like: who's providing what, what your rating gets you, and what to do before you use.

Lenders advertise the flooring; the majority of debtors land somewhere in the middle. Understanding your tier upfront tells you whether to shop aggressively today or invest 90 days improving your rating. Credit ScoreTypical APR RangeMonthly Payment: $10,000/ 36 moTotal Interest Paid760+ (Excellent)7%11%$309$328/mo$1,124$1,808700759 (Great)12%17%$332$356/mo$1,952$2,816650699 (Fair)18%24%$362$391/mo$3,032$4,076600649 (Poor)25%32%$400$431/mo$4,400$5,516 Below 60033%36% (or rejected)$443$454/mo$5,948$6,344 The majority of Americans being in the 650720 FICO variety.

Online loan providers and credit unions consistently beat Chase and Wells Fargo on individual loan rates. Best for big loans between $25,000 and $100,000 with no origination costs.

Why Variable Rates May Be Risky for Your StateCritical Steps to Reducing Interest Payments Via Management

Rates from 8.99%25.81% APR. Targets customers making $75,000+ with solid credit. Rates from 6.99%24.99% APR.

Charges an origination cost of 3%8%, which you require to factor into your efficient cost. That fee at the high end on a $15,000 loan adds $1,200 upfront always compare the APR, not the specified rate. Caps individual loan APR at 18% for members. If you or a household member has military or DoD ties and you're bring card financial obligation above 18%, check eligibility initially.

{kind=link}

Latest Posts

Leveraging Loan Estimation Tools for 2026

Evaluating Debt Relief Solutions for Future Stability

Is Debt Management Best for You in 2026?